We recently came across a column by Professor Gregory Clark of UC Davis entitled Family Wealth that challenged and frankly reshaped how we think about generational wealth. (A hat tip to Verdad Capital for surfacing this fascinating piece.) We encourage you to read the article in full. Here are a few key takeaways that stood out to us.

First, inherited financial wealth rarely endures. As Andrew Carnegie famously observed, “shirtsleeves to shirtsleeves in three generations.” The arithmetic is unforgiving as wealth is divided among heirs and further diminished by taxes, costs, and spending.

Second, and more surprisingly, Clark’s broader body of work, including his book The Son Also Rises, shows that underlying family success persists far longer than most assume. Yes, financial capital erodes. But human capital and social competence along with shared values and behaviors, plays the central role in shaping outcomes across generations. In research spanning four centuries of British families, with supporting evidence from 19th century America and post-Communist China, Clark finds that descendants tend to maintain above average wealth not because of inherited financial assets, but because of inherited capability.

As he puts it:

“Judgment, discipline, curiosity, and ambition: these are the true endowments. Families that endure understand, whether explicitly or not, that where their treasure is laid up is not in accounts or trusts, but in the character and capability of their children and grandchildren and great-grandchildren.”

We found the concept so compelling that we reached out to Professor Clark to learn more. He was kind enough to respond to our follow-up questions, which we felt have practical implications for your children/grandchildren (and ours):

Question: For affluent families thinking about their children, what lessons should they take from your research? Are there specific traits, behaviors, or forms of “capital” that seem most important in sustaining success across generations?

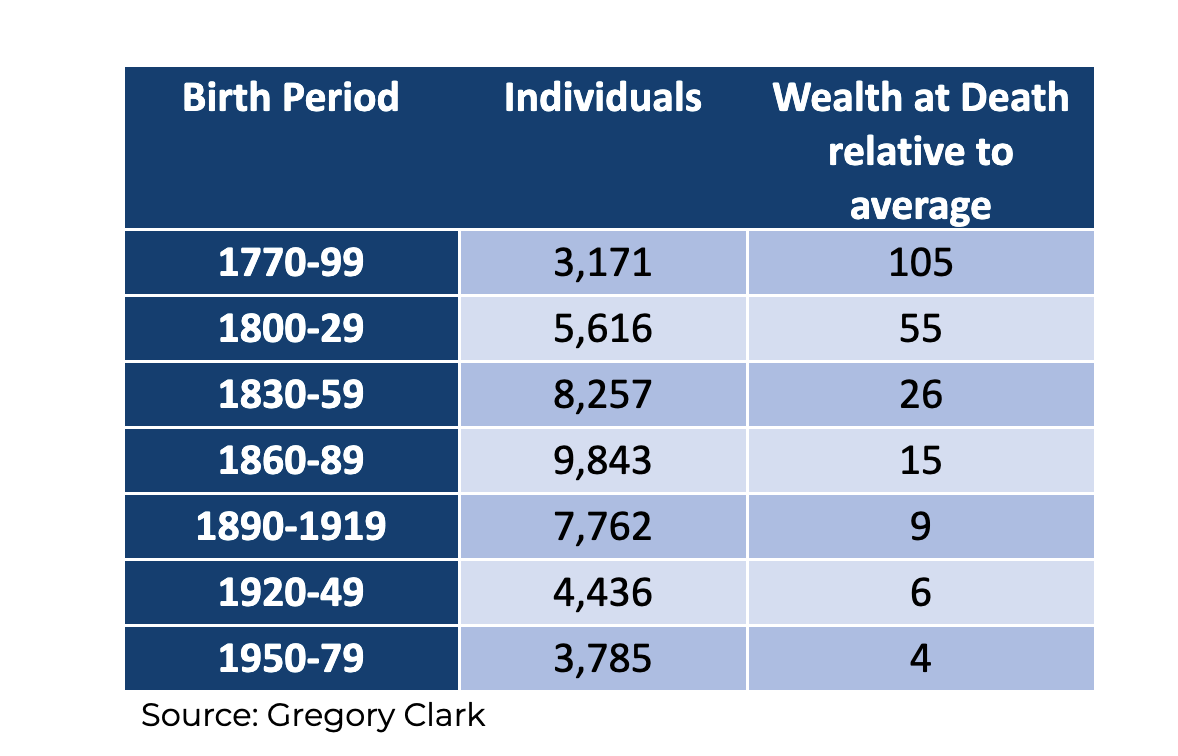

Professor Clark: Based on the histories of a large group of initially wealthy English families 1770-2026, we see the pattern below in terms of wealth at death across time.

The first lesson is that for the wealthy as a group, wealth always regresses to the mean. But it does so at modest pace. The original wealthy born 1770-99 will still have descendants, for those born 1950-1979, four times as wealthy as the average.

We see in the data, however, that the families that succeeded best in holding on to wealth were those that produced children of the highest education or occupational level.

Another key component of wealth persistence was the marriages the children made. Fathers and mothers were equally predictive of the educational and occupational attainment of their children. So children who married spouses from higher ability families saw more persistence in wealth and other measures of status by their offspring than did children who married partners of lower social status.

Question: Your work often points to a kind of persistent “underlying social competence” that transcends wealth alone. How should families think about developing that in their children?

Professor Clark: While “social competence” in the English data is strongly inherited, the data actually suggests that this inheritance was largely determined at birth.

Since social abilities, however, derive equally from fathers and mothers, the key determinant of the abilities of children that families can control were marital partners. Families that persisted as wealthy did so because of the succession of successful marriages that their children, grandchildren, and great grandchildren made.

An example of a family which had extraordinary success in terms of wealth and social position in England was the Pepys family, who had elite status from the 17th century onwards. But modern holders of the Pepys surname have only a tiny fraction of their DNA that derives from their original Pepys male ancestor. The vast bulk of the DNA of modern Pepys comes from the long succession of successful marriages made by the Pepys sons over the years 1600-2000.

Question: Conversely, what are the most common mistakes you see families make when trying to preserve wealth across generations?

Professor Clark: The only obvious financial mistake of English wealthy families was a tendency to invest too much in prestige assets, which in their case was country estates. Post 1870 and the invasion of cheap food and raw materials from the New World, rural land values in England stagnated or declined.[i]

In Conclusion

We’re grateful for both Professor Clark’s work and elaboration. Preserving and compounding wealth is not just about investment returns. This notion is a big part of why we started Flatrock. Human capital – the present, after-tax value of future earnings – for most of our clients remains their largest asset, often well into their 50s and early 60s. Of course, the younger a client or their child, the more of a factor human capital, not financial capital, has in shaping financial outcomes.

Additionally, as Professor Clark referenced, fees and taxes are a big part of the degradation in inherited financial wealth. The minimization of both is a cornerstone of how we approach wealth management. But advisors seldom build human capital into the financial plan or accompanying investment strategy. And precious few make fees and taxes primary focus areas.

[i] One wonders what assets today might be considered “prestige assets.” Given the high costs and poor tax efficiency of many alternative asset classes, we wonder whether these may, in the decades ahead, be similarly viewed as a common source of wealth erosion.